import numpy as np

import matplotlib.pyplot as plt

from stable_baselines3 import SAC

from stable_baselines3.common.monitor import Monitor

from stable_baselines3.common.callbacks import BaseCallback

from common import (

ornstein_uhlenbeck,

TradingEnv,

buy_and_hold,

evaluate_policy_on_env,

sharpe_ratio,

max_drawdown,

plot_learning_curve,

plot_equity_curves,

plot_price_and_positions,

)

SEED = 0

TRAIN_SEED = 1

TEST_SEED = 999

N_TRAIN = 5000

N_TEST = 3000

WINDOW = 20

COST = 0.0005

TOTAL_STEPS = 60_000Lesson 7 — Continuous position SIZING with SAC

Every agent so far chose a direction: short, flat, or long — three discrete buttons. But a real desk does not just decide which way; it decides how much. Half a unit of conviction should buy half a position. Sizing is risk control, and it is where FX trading actually lives. So we replace the three buttons with a continuous dial: a target position anywhere in [-1, +1].

That one change breaks DQN. DQN works by taking argmax over actions — trivial when there are three, impossible when there are infinitely many points in an interval. Continuous control needs a different algorithm class: an actor-critic that outputs an action directly instead of scoring a finite menu.

Enter SAC: Soft Actor-Critic

SAC (Soft Actor-Critic) is an off-policy actor-critic for continuous control. It keeps two moving parts:

- an actor (the policy) that maps a state to a distribution over actions and samples the position to take, and

- a critic (a Q-network, in fact two of them, to fight over-optimism) that scores how good a (state, action) pair is.

Its defining trick is maximum-entropy RL: SAC maximises reward plus the policy’s entropy. In plain terms it is rewarded for staying as random as it can get away with while still succeeding. That built-in pressure to stay stochastic makes it explore thoroughly, learn from a replay buffer sample- efficiently, and end up robust rather than brittle. An automatically tuned “temperature” trades entropy off against reward as training proceeds.

The deterministic cousins

DDPG and TD3 solve the same continuous-control problem with a deterministic actor (one action, no distribution) plus hand-added exploration noise. TD3 is essentially DDPG made stable (twin critics, delayed updates). SAC’s entropy bonus usually makes it the more forgiving default — and it is the algorithm class we reach for in the FX capstone.

We train on one mean-reverting Ornstein-Uhlenbeck path and, as always, judge the agent only on a held-out path it has never seen.

Run order matters. The cells below build on each other. Run them top to bottom (Jupyter: Run → Run All Cells; VS Code: Run All). If you hit

NameError(or similar), you skipped the Setup cell — run it first.

Setup — imports & configuration

Run this cell first. It imports every library and defines the module-level constants the rest of the notebook relies on.

RewardLoggerCallback (class)

Collect per-episode rewards from the Monitor wrapper during training.

Stable-Baselines3’s Monitor writes a summary dict into info["episode"] the moment an episode ends ("r" = total reward, "l" = length). This callback fires on every environment step, watches the infos that SB3 exposes in self.locals, and stashes each finished episode’s reward. That growing list is our learning curve — the honest record of whether training is improving the policy or just burning GPU cycles.

class RewardLoggerCallback(BaseCallback):

def __init__(self):

super().__init__()

self.episode_rewards = []

def _on_step(self):

for info in self.locals.get("infos", []):

episode = info.get("episode")

if episode is not None:

self.episode_rewards.append(episode["r"])

return Truemake_prices (function)

One mean-reverting Ornstein-Uhlenbeck price path from a given seed.

The seed is the whole point: calling this with two different seeds gives two statistically similar but independent markets. We train on one and test on the other — the only honest way to ask “did the agent learn a rule, or memorise a path?”.

def make_prices(n, seed):

rng = np.random.default_rng(seed)

return ornstein_uhlenbeck(n, rng, mu=1.0, theta=0.05, sigma=0.01)train_sac (function)

Train a SAC agent on the continuous-action training environment.

These are standard SAC settings for a small MLP on a dense reward:

learning_rate=3e-4— the usual Adam step for both actor and critics.buffer_size=100_000withlearning_starts=1000— SAC is off-policy, so it replays a large pool of past transitions; fill it a little before training so early gradients are not dominated by one trajectory.batch_size=256— big minibatches keep the critic updates low-variance.gamma=0.99— value future PnL almost as much as present PnL.tau=0.005— Polyak coefficient; the target critics track the live critics slowly, which is what keeps bootstrapped values from diverging.train_freq=1,gradient_steps=1— one gradient update per env step, the setting that makes SAC so sample-efficient.

The entropy temperature is auto-tuned by default, so we do not set it: SAC decides for itself how stochastic to stay. Returns the trained model and the list of per-episode training rewards.

def train_sac(train_env, total_steps, seed):

logger = RewardLoggerCallback()

model = SAC(

"MlpPolicy",

train_env,

learning_rate=3e-4,

buffer_size=100_000,

learning_starts=1000,

batch_size=256,

gamma=0.99,

tau=0.005,

train_freq=1,

gradient_steps=1,

device="auto",

seed=seed,

verbose=0,

)

model.learn(total_timesteps=total_steps, callback=logger, progress_bar=False)

return model, logger.episode_rewardsreport_metrics (function)

Print the three numbers a trader actually judges a strategy by.

def report_metrics(label, metrics):

print(

f"{label:14s} | total PnL = {metrics['total_pnl']:+.4f} "

f"| Sharpe = {metrics['sharpe']:+.2f} "

f"| max drawdown = {metrics['max_drawdown']:+.4f}"

)plot_position_histogram (function)

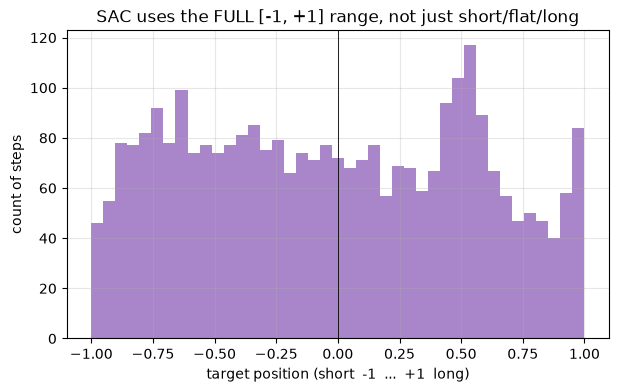

Histogram of the continuous positions the agent chose.

This is the figure that proves the point of the whole lesson. A discrete agent can only ever land on -1, 0, or +1, so its histogram would be three spikes. A continuous agent that has genuinely learned to size spreads its mass across the whole [-1, +1] dial — scaling how much it holds with how confident it is, not just picking a direction.

def plot_position_histogram(positions, title="Agent position sizes (held-out)", ax=None):

if ax is None:

_, ax = plt.subplots(figsize=(7, 4))

ax.hist(positions, bins=41, range=(-1.0, 1.0), color="tab:purple", alpha=0.8)

ax.axvline(0, color="k", lw=0.6)

ax.set_xlabel("target position (short -1 ... +1 long)")

ax.set_ylabel("count of steps")

ax.set_title(title)

ax.grid(alpha=0.3)

return axmain (function)

def main():

np.random.seed(SEED)

# --- Build TRAIN and HELD-OUT TEST markets from DIFFERENT seeds ---------

train_prices = make_prices(N_TRAIN, TRAIN_SEED)

test_prices = make_prices(N_TEST, TEST_SEED)

print(

f"Train path: {N_TRAIN} bars (seed {TRAIN_SEED}) | "

f"Held-out test path: {N_TEST} bars (seed {TEST_SEED})"

)

# Continuous action space + a risk-adjusted (Sharpe) reward. Monitor wraps

# the training env so finished-episode rewards are logged for the curve.

train_env = Monitor(

TradingEnv(train_prices, window=WINDOW, cost=COST,

continuous=True, reward="sharpe")

)

# --- Train ------------------------------------------------------------

print(f"\nTraining SAC for {TOTAL_STEPS:,} steps (device=auto)...")

model, episode_rewards = train_sac(train_env, TOTAL_STEPS, SEED)

print(f"Done. Logged {len(episode_rewards)} training episodes.")

# --- Evaluate on the HELD-OUT test path -------------------------------

# Fresh continuous env on the test prices: never-before-seen returns.

test_env = TradingEnv(test_prices, window=WINDOW, cost=COST,

continuous=True, reward="sharpe")

agent = evaluate_policy_on_env(model, test_env, deterministic=True)

# Buy-and-hold (always +1) on the SAME held-out env is the baseline to beat.

bh_env = TradingEnv(test_prices, window=WINDOW, cost=COST,

continuous=True, reward="sharpe")

bh_pnls = buy_and_hold(bh_env)

bh_metrics = {

"total_pnl": float(np.sum(bh_pnls)),

"sharpe": sharpe_ratio(bh_pnls),

"max_drawdown": max_drawdown(bh_pnls),

}

print("\nHeld-out test performance:")

report_metrics("SAC agent", agent)

report_metrics("buy & hold", bh_metrics)

positions = np.asarray(agent["positions"], dtype=np.float64)

print(

f"\nAgent position range: [{positions.min():+.2f}, {positions.max():+.2f}]"

f" | mean |position| = {np.abs(positions).mean():.2f} "

f"(a discrete agent could only ever print -1, 0, or +1)"

)

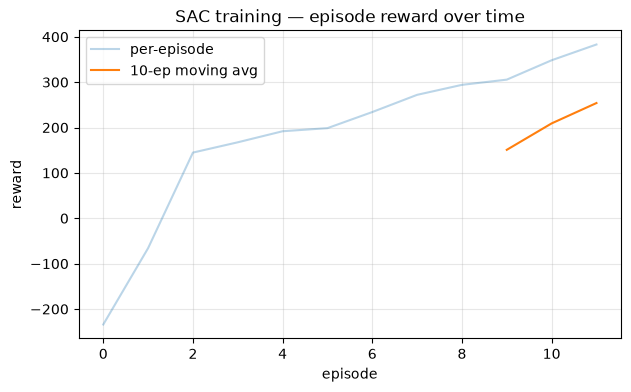

# --- Figure 1: learning curve -----------------------------------------

plot_learning_curve(

episode_rewards, window=10,

title="SAC training — episode reward over time",

)

plt.show()

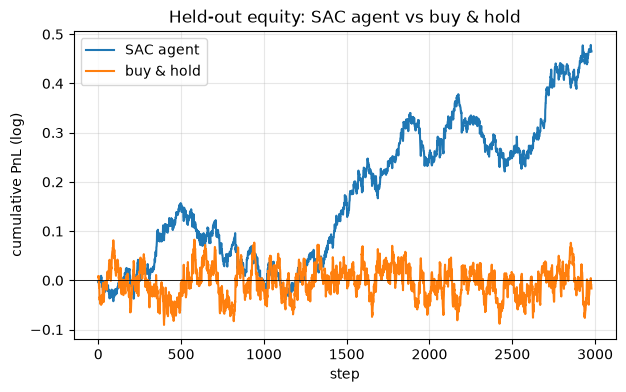

# --- Figure 2: equity curves on held-out data -------------------------

plot_equity_curves(

{"SAC agent": agent["pnls"], "buy & hold": bh_pnls},

title="Held-out equity: SAC agent vs buy & hold",

)

plt.show()

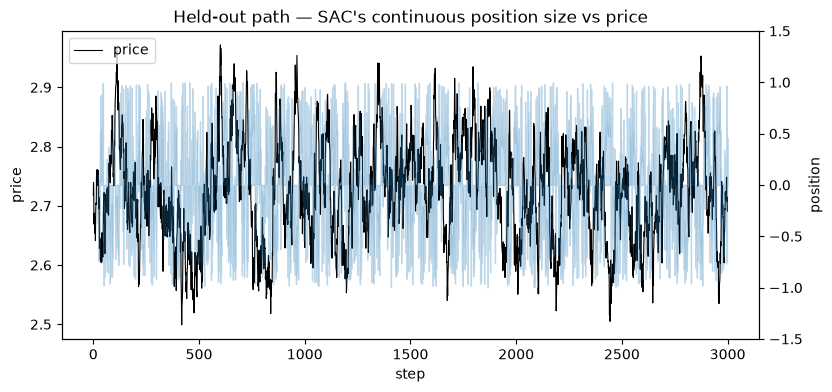

# --- Figure 3: the CONTINUOUS position varying smoothly with price ----

plot_price_and_positions(

test_prices, agent["positions"],

title="Held-out path — SAC's continuous position size vs price",

)

plt.show()

# --- Figure 4: the histogram that proves it uses the whole dial -------

plot_position_histogram(

agent["positions"],

title="SAC uses the FULL [-1, +1] range, not just short/flat/long",

)

plt.show()

# --- Takeaway ---------------------------------------------------------

print(

"\nTakeaway: making the action a continuous target position turns "

"direction-picking into position SIZING — the agent scales how much it "

"holds with its conviction, which is the essence of risk control. DQN "

"cannot do this (there is no argmax over a continuous interval), so we "

"switched to SAC: an off-policy actor-critic that maximises reward PLUS "

"policy entropy, exploring by staying as stochastic as it can while still "

"succeeding. That makes it sample-efficient and robust. DDPG/TD3 are its "

"deterministic cousins. Watch the position histogram: the mass spread "

"across [-1, +1] is the whole point — and SAC is the algorithm class we "

"carry into the FX capstone."

)Run the lesson

Execute everything above, then run main().

main()Train path: 5000 bars (seed 1) | Held-out test path: 3000 bars (seed 999)

Training SAC for 60,000 steps (device=auto)...

Done. Logged 12 training episodes.

Held-out test performance:

SAC agent | total PnL = +0.4650 | Sharpe = +0.45 | max drawdown = -0.1892

buy & hold | total PnL = -0.0165 | Sharpe = -0.01 | max drawdown = -0.1720

Agent position range: [-1.00, +1.00] | mean |position| = 0.49 (a discrete agent could only ever print -1, 0, or +1)

Takeaway: making the action a continuous target position turns direction-picking into position SIZING — the agent scales how much it holds with its conviction, which is the essence of risk control. DQN cannot do this (there is no argmax over a continuous interval), so we switched to SAC: an off-policy actor-critic that maximises reward PLUS policy entropy, exploring by staying as stochastic as it can while still succeeding. That makes it sample-efficient and robust. DDPG/TD3 are its deterministic cousins. Watch the position histogram: the mass spread across [-1, +1] is the whole point — and SAC is the algorithm class we carry into the FX capstone.